The GPN Trap

Trading at 6x earnings, $GPN appears cheap, but structural shifts loom. Explore how the $24B Worldpay merger and legacy tech stack are transitioning the company from a growth into utility.

The thing about value traps is they all feel the same. Too cheap, too beaten down, and too good to pass up. And for the payments people, one of the more popular potential value traps today is Global Payments (GPN), beaten down 30% YTD and trading around 6 or 7 times forward earnings.

Before I get into it, what do you think?

To figure out if this is a cheap compounder or a value trap, you need to go back to basics on how we all make money in investing. You buy something, it goes up in price, you sell or have an unrealized gain. But why does a stock go up? Typically, one of two things happen. One, fundamentals improve and the company produces more revenue, earns more money, and grows its value intrinsic value, or some combination of the all three. Two, people’s perception of the stocks future value go up. The CFA explanation for this is called “the multiple” and it can come in the form of a P/E, an EV/EBITDA, EV/Sales, P/S, and many others. But the uniting force across all of these multiples is that more people must be willing to pay more for the stock than it’s otherwise worth today.

Investing bliss is when these things work in tandem; fundamentals improve way more than what people think and all of a sudden people start paying even more than what the company should be worth. Or put simpler, people start to think its future is better than it’s past. This is what happened with the AI complex over the past 2-3 years.

But value traps all violate this truth. They should be worth more, but they’re not. And from experience, value traps will become lead weights on your future returns. Especially because you become convinced that everyone else has it wrong while it just sits there, not moving, sucking performance from you and becoming a mental drain in the process.

With GPN I think the cards are stacked against you and that it is going to be way too hard for this stock to break out of value trap status. I wouldn’t short it but I also wouldn’t buy it and here are the reasons why.

A Mature & Utility Like Business Model With a Tech Wrapper

Yes GPN did about $9b in adjusted net revenue last year which was 6% YoY growth. And yes adjusted EPS was $11.55 up about 11%. And yes 2025 guidance calls for the year finishing the year up about 6% on revenue and 11% on EPS with very tentative 2026 EPS growth in the “mid teens”. It’s trading around 6x earnings, definitionally cheap. But remember GPN makes their money predominantly from Merchant Solutions. This is the financial service that enables businesses to accept credit and debit card payments by handling the authorization of transactions and settling the funds into the merchant’s bank account. All this is code for payments volume. And this is a mega thin margin business model.

And in reality this is what a utility looks like. Stable, low growth, profitable, and not sexy at all. At it’s core, the merchant acquiring that GPN does is a handful of basis point type commodity on someone else’s rails. It is governed by a Visa or Mastercard, it is limited by what I call “take-rate gravity” meaning you can’t charge more without losing merchants, and it is inherently tied maybe 70% or 80% to nominal PCE and inflation. More payments, more scrape revenue.

To command a premium multiple, not a 6x P/E, a fintech needs 15% to 20% revenue growth fueled by product innovation, pricing power, and platform lock-in. GPN has none of these; it is officially the Boomer of the payments world. Mature, safe, and utility like. Now ask yourself, does this type company deserve a premium multiple?

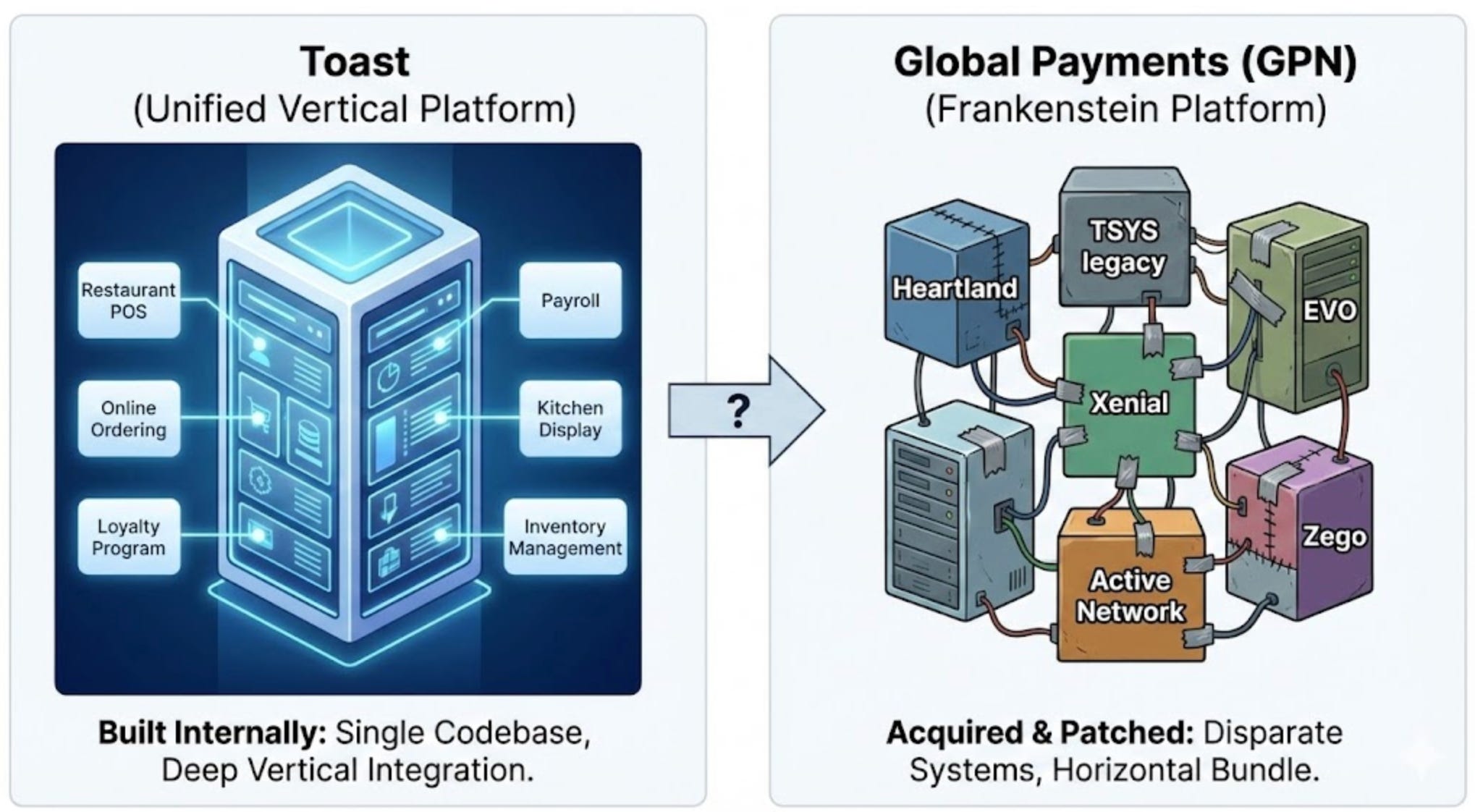

The Frankenstein Tech Stack Challenge Compared to Competitor’s Unified Ecosystem

The next challenge is that GPN’s competitors are self listed as Fiserv (Clover), FIX, Stripe, Adyen, Chase, Paymentech, and Elavon. They also compete to a lesser degree with Toast and Shift4. It is a crowded space with everyone competing for a piece of the payments pie.

But structurally, GPN is fighting with one hand tied behind its back. GPN’s platform is a Frankenstein composed of acquired pieces: Heartland, TSYS legacy, EVO, Xenial, Active Network, Zego, etc. Nowhere does GPN claim to offer a single, modern, developer-first global platform the way Stripe and Adyen do. While Stripe and Adyen spent a decade building a unified global system from scratch, GPN spent its time stitching together disparate regional systems through M&A.

On the restaurant side, a minor revenue segment for GPN but a perfect illustration of the problem, Toast wins because it functions as the restaurant’s entire operating system. It integrates inventory, payroll, and orders into one “sticky” platform that is painful to rip out. In contrast, Global Payments is often treated as merely the interchangeable plumbing that moves money from point A to point B. By owning the workflow rather than just the transaction, Toast gains deep data visibility and pricing power that a commodity processor simply cannot match.

What does GPN win on? M&A, distribution, management execution, and salesforce persistence. They do not win on “product-first” gravity. Again, this isn’t meant to be insulting, just a statement of structural difference. GPN is a scaled, very competent operator, not a “why customers rave about us” innovator. In modern payments, UX is the sizzle that gets you a premium multiple because it gives you the potential for a moat in the future if you can win a space.

And what’s the last piece of the puzzle on GPN?