I'm Popular Now: How a Boring Bank Beat the Market

This one’s for the newer readers who aren’t familiar with Victaurs’ bank game. And while it may seem like boasting, the key to improving as an investor and fund manager or capital allocator is looking back to see if you did any good. And if you read on you’ll get exactly what went right but also, a screen in the bank space for names that have the same set up as this winner from last year. They’re formatted to show you who is top tier and who is not in bank land. If you’re serious about banks, the screen alone will pay for your subscription and help you avoid some landmines.

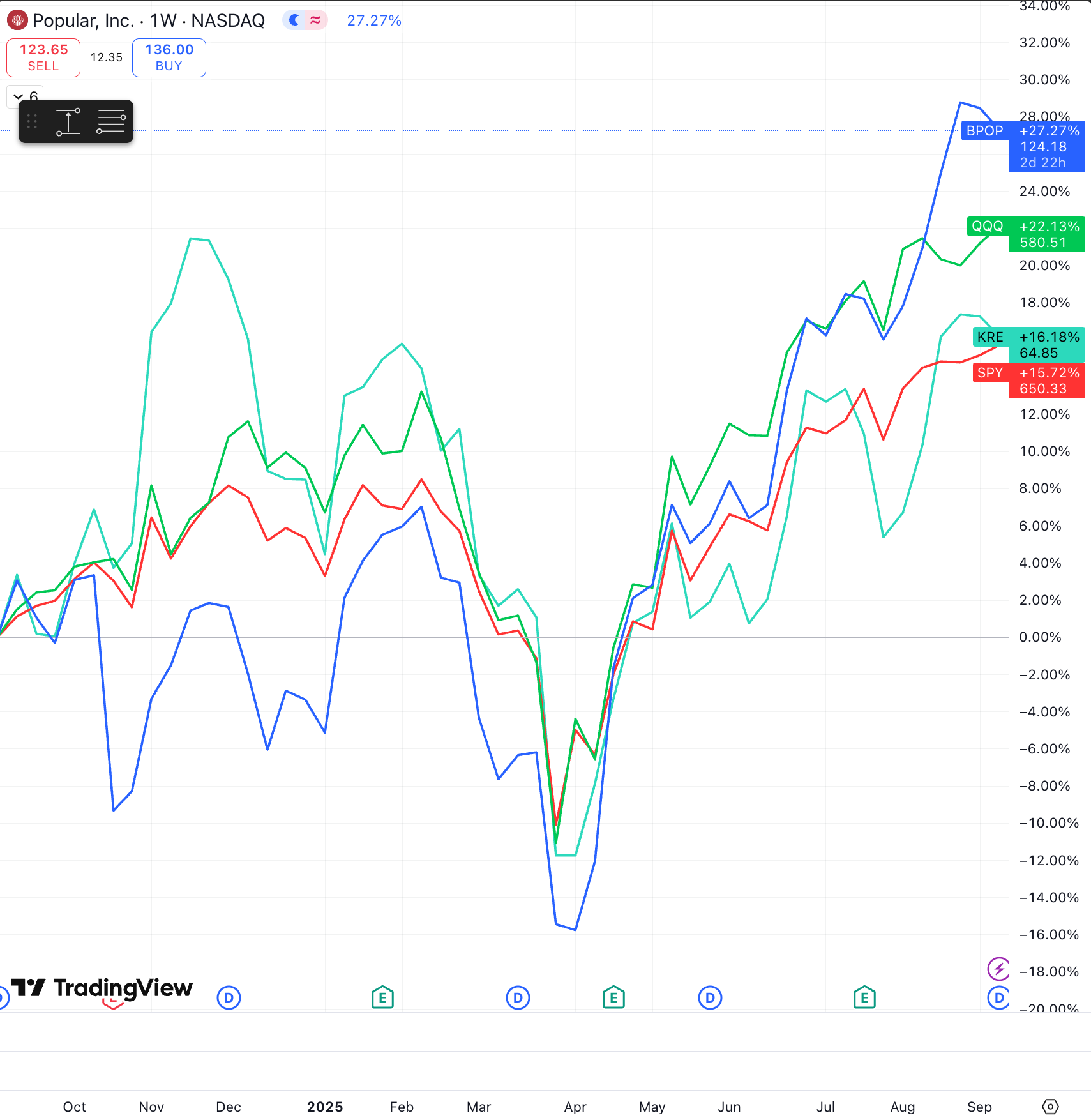

On 9/9 of last year I wrote up Popular (BPOP) and set a fair value band somewhere in the $115 to $125 range, with a bull case up towards $130-$135.

It’s funny to look back because you also get a lens into your psyche at the time of trades and investments. Back then I was kicking myself for seeing it, and not buying in when it was trading at $60 or $70. Fast forward to today and we got to $125 a few months earlier than expected. And it was done quietly, cleanly, and without drama I might add despite the siren calls of the bank doomers constantly jawboning about unrealized losses and CRE modificiations. But what you may not know is that this one actually beat the SPY, QQQ, and also the regional bank ETF KRE. BPOP was up 27% while QQQ did about 22%, KRE was up about 16%, and SPY 16% also. Even Wells Fargo’s latest research now echoes the framework I laid out back then, and they even gave a nod to Bad Bunny like I did.

For bank investors, the core idea was simple. Buy sleepy almost mechanical EPS growth at a beaten down multiple that no one was paying attention to. And I mean no one. The thing was barely noticed back then. Part of the mispricing came from positioning too, people basically just ignored Puerto Rico names.

But for me, the earnings trajectory was the tell. It’s a reminder that sometimes the cleanest setups are hiding in plain sight, simplicity is often the edge. 2024 EPS near $9 put you at roughly 11x. Street numbers for 2025 pointed to the low $11 range, which implied low 20% EPS growth at around 9x forward. Something did not add up because that is a multiple the market usually reserves for stalled franchises, not for a company stepping up earnings at that clip.

And now? Well now things look just as interesting. And behind the wall too is a screen on which banks have outsized 2026 EPS growth with cheap valuations.

Keep reading with a 7-day free trial

Subscribe to Victaurs to keep reading this post and get 7 days of free access to the full post archives.